Client

Our client runs a financial services business. They operate as a broker company and offer trading and investment services, helping customers to invest in and manage asset portfolios like forex pairs, metals, CFD commodities or cryptocurrencies.

Challenge

The client had a functioning electronic trading platform of the MetaTrader kind. As in most cases, this type of platform has significant restrictions for broker companies. It is used primarily for account creation and funding and has only rudimentary referral capabilities.

Our client wanted to expand its trading platform with multi-account management module (MAM) and percentage allocation management module (PAMM) functionality. They also needed to implement a multi-tier, and progressive-based referral system with automatic rewards.

It is a classic situation that requires the development of custom financial software. It is one of our specializations, so the customer has contacted us.

Solution

MAM Module

This module is the primary method for managing investor funds. This is a system where a trader manages the funds of several clients on a single platform. Funds remain in the clients' accounts, in compliance with the legislation of various countries.

Copy Trading Module

MAM accounts are used by clients who wish to adopt the trading strategies of their selected traders.

Our client, a broker, interacts with traders primarily through the basic functions of an electronic trading platform. The broker works with traders who have proven trading strategies and wish to manage other clients' money in exchange for a commission. Initially, the platform did not support copy trading. We have since integrated these capabilities.

Previously, traders had to log out of the investor's account and log into the account they were managing.

Now, the MAM module automatically initiates trades of the desired volume on all accounts linked with a trader. A trader just needs to make a purchase from their own account.

Example of an effective strategy

Risk Management Module

The risk management module allows each investor to set their own risk multipliers (corrective coefficients) and includes loss limiters. They automatically stop the account from following the trading strategy if equity falls to a specified level. This feature is highly attractive to investors.

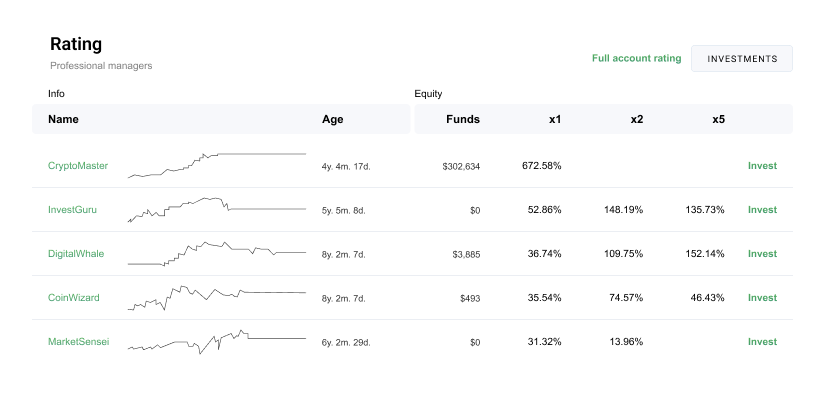

Now, the investors can choose from a list of traders who offer the best trading strategies

PAMM Module

We developed and integrated the PAMM module into the platform.

Now, the funds from an unlimited number of clients can be pooled into a single trading account under the management of a trader.

The module has created the ability to automatically distribute returns to investors according to their contributions.

Analytic Instruments

We developed customized tools that provide real-time statistics for managed accounts, and offer detailed insights into the investments. They include a lot of metrics like TWR% (Total/Daily/Monthly/Custom range), Drawdown %, Profit Factor, Expectancy (% and pips), Average Trade Duration, Standard Deviation, Volatility, Sharpe Ratio, Correlation between strategies etc.

This tool also allows investors to understand how strategies correlate and implement strategies with little connection to one another, which decreases risks. Consequently, if one strategy does not perform as expected, it will not significantly impact the entire portfolio, leading to more stable overall portfolio performance.

CRM System

We expanded the capabilities of the broker. They now have a tailored CRM system that allows for the management of traders, investors, and transaction lists. We also customized the referral and reward system. It now automatically calculates and distributes fees using a multi-level, progressive system based on parameters that a broker can set. Traders use this referral and reward system to invite new investors, contributing to the growth of the customer base and increasing investment volumes.

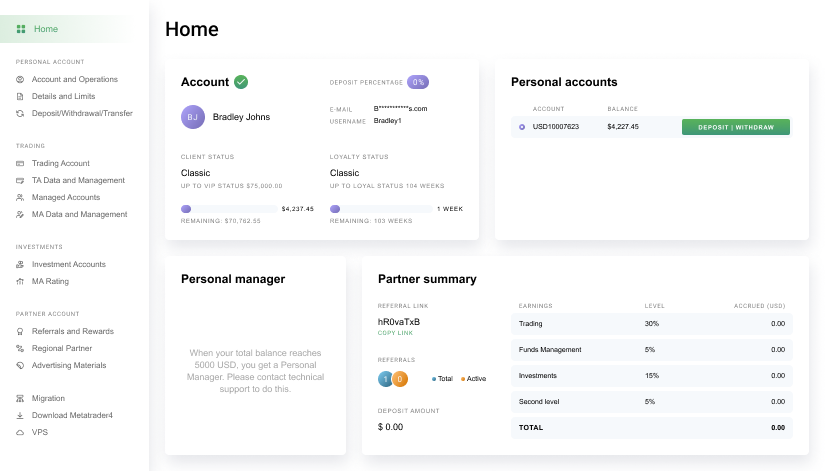

Personal Investor/Trader Dashboard

We developed a personal dashboard where users can make investments, request withdrawals, and fund their accounts with credit cards without invoices

A trader-specific dashboard was also developed to facilitate registration and immediately start trading.

Results

The client can now attract new traders and investors to their platform at scale. Analysts of investing.co.uk rated platform's unique features very highly when compared to other forex brokers. They appreciated the simple registration process and were pleased to see that the system integrates with MetaTrader 4, offers a demo account, and supports copy trading. They were impressed by the focus on risk management, where investors can establish loss limits, and by the ability to manage multiple accounts under one manager with varying degrees of control.

Related cases

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

Recommended posts

.png)

.jpg)

.jpg)

.png)

Our Clients' Feedback

Belitsoft has been the driving force behind several of our software development projects within the last few years. This company demonstrates high professionalism in their work approach. They have continuously proved to be ready to go the extra mile. We are very happy with Belitsoft, and in a position to strongly recommend them for software development and support as a most reliable and fully transparent partner focused on long term business relationships.

Global Head of Commercial Development L&D at Technicolor

They use their knowledge and skills to program the product, and then completed a series of quality assurance tests. We were working in an agile way with them. Belitsoft performed very well throughout our project. We are definitely looking at Belitsoft as a long-term partner.

Service Delivery Director at Crimson (United Kingdom)

I highly recommend Belitsoft for website design and development. We were up against a tight deadline to launch the project. The work was delivered on time and within budget! I will continue working with Belitsoft as a valued partner for our web development!

Program Administrator at UC Berkeley (United States)

We have worked with Belitsoft team over the past few years on projects involving much customized programming work. They are knowledgeable and are able to complete tasks on schedule, meeting our technical requirements. We would recommend them to anyone who is in need of custom programming work.

Main Partner at Hathway Tech (United States)

Belitsoft company is able to make changes instantly. One of our internal engineers has commented about how clean their code is. Belitsoft seems to know what they're doing, which I appreciate.

Co-Founder at HOWCAST MEDIA (United States)

It was a great pleasure working with Belitsoft software development company. New requirements and adjustments were implemented fast and precisely. We can recommend Belitsoft and are looking forward to start a follow-up project.

Head of Division at Fraunhofer FIT (Germany)

Belitsoft company has been able to provide senior developers with the skills to support back end, native mobile and web applications. We continue today to augment our existing staff with great developers from Belitsoft.

CEO at Apollo Matrix (United States)

Belitsoft company delivered dedicated development team for our products, and technical specialists for our clients' custom development needs. We highly recommend to use this company if you want the same benefits.

Managing Director at Key2Know A/S in 2012 (Denmark)

We approached BelITsoft with a concept, and they were able to convert it into a multi-platform software solution. Their team members are skilled, agile and attached to their work, all of which paid dividends as our software grew in complexity.

COO at Regenerative Medicine LLC (United States)

Having worked with Belitsoft as a service provider, I must say that I'm very pleased with the company's policy. Belitsoft guarantees first-class service through efficient management, great expertise, and a systematic approach to business. I would strongly recommend Belitsoft's services to anyone wanting to get the right IT products in the right place at the right time.

CEO at Moblers

If you are looking for a true partnership Belitsoft company might be the best choice for you. They have proven to be most reliable, polite and professional. The team managed to adapt to changing requirements and to provide me with best solutions. I strongly recommend Belisoft.

Director at ShowCast Limited (Germany)

I expected and demanded a lot of you at Belitsoft company, but you exceeded my expectations. You acted pro-actively, challenged me at the right moments. Thanks!"

CEO at Ticken B.V. (Netherlands)

We have been working for over 10 years and they have become our long-term technology partner. Any software development, programming, or design needs we have had, Belitsoft company has always been able to handle this for us.

Founder from ZensAI (Microsoft)/ formerly Elearningforce